6 / 62

6 / 62

A D V A N C E D M A T E R I A L S & P R O C E S S E S | M A R C H 2 0 1 5

6

MARKET SPOTLIGHT

FEEDBACK

THE JOY OF STAINLESS

I thoroughly enjoyed the recent ar-

ticle on stainless steels (“Metallurgy

Lane,” January). I am a metallurgist

by training and have been asked to

prepare a presentation on stainless

steels for UTC Aerospace Systems’

personnel. I am also interested in

any other information, articles, or

presentations that the author might

be willing to share on the subject.

Robert Bianco, FASM

[

AM&P

supplied an advance copy of “Stain-

less Steel: Part II” from the February issue

for use in Dr. Bianco’s presentation.—Eds.]

ALUMINUM ALLOYS

I immensely enjoy the “Metallur-

gy Lane” articles in

AM&P.

I am a

student of the history of aluminum,

and I live in one of the most import-

ant areas for the production of early

aluminum products, Manitowoc,

Wis. I just wanted to point out what

I believe to be an oversight in Part III

of the aluminum series, published

in Nov/Dec 2014. In this article, the

2000 series is identified as alumi-

num-magnesium alloys. However,

I believe these are conventionally

referred to as aluminum-copper

alloys.

David Weiss

[Weiss is correct in that the 2000 series is

reserved for the Al-Cu alloys, but 2024 must

include Mg. I should have said Al-Cu-Mg

alloys.—Charles R. Simcoe]

We welcome all comments and

suggestions. Send letters to

frances. richards@asminternational.org.

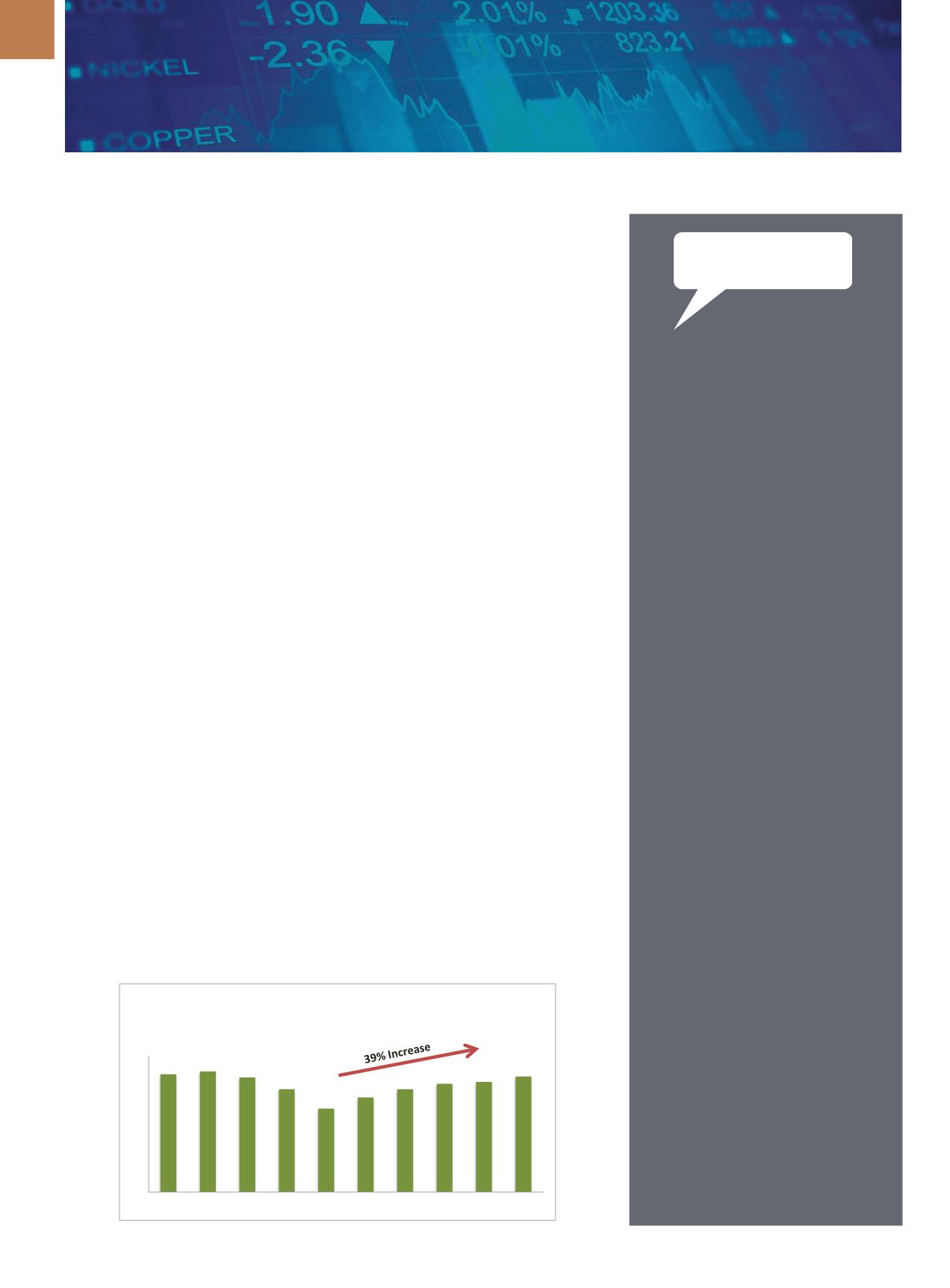

NORTH AMERICAN ALUMINUM INDUSTRY

SHOWS SUSTAINED GROWTH

According to preliminary data re-

leased in the Aluminum Association’s

monthly

Situation Report,

the aluminum

industry in the U.S. and Canada experi-

enced year-over-year demand growth

of 5% through the end of 2014. The

estimated 25.5 billion lb of aluminum

shipped by North American producers

and fabricators last year is the largest

shipment total for the industry since

2006, say analysts. Key findings include:

•

Apparent aluminum consumption

(demand minus exports) in do-

mestic markets totaled 22 billion lb

through the end of 2014, a 7.3%

increase over 2013.

•

Total mill product shipments grew

4.5% in 2014, led by growth in

extrusion, foil, and sheet and plate

markets.

•

New orders of aluminummill prod-

ucts rose 3.9% in 2014 and were up

3% in January year-over-year.

•

Secondary recovery—or recycling—

of aluminum is up 4.1% year-to-date

through November 2014 (U.S. only).

•

Primary aluminum production de-

clined 7.1% in 2014 and was down

4% year-over-year in January.

•

Imports of aluminum (excluding

U.S./Canada cross-border trade)

rose 20.2% in 2014 to 5.5 billion lb,

while exports declined 6.8% to

7.4 billion lb.

“Growth in North American de-

mand for aluminum in 2014 is even

more impressive given the harsh winter

weather the region experienced at the

start of the year, and the significant im-

pact it had on operations,” says

Ryan

Olsen

, vice president of business infor-

mation and statistics for the Aluminum

Association. “Demand grew just eight-

tenths of one percent year-over-year

during the first four months of 2014,

compared to a year-over-year increase

of 7.1% over the final eight months.”

According to the latest data, alumi-

num demand has grown by 38.3% since

the depths of the Great Recession in

2009 and continues to expand. Over the

past two years, Aluminum Association

member companies have announced

domestic plant expansions and planned

investments totaling more than $2.3

billion. Investments are intended to

meet anticipated demand growth for

aluminum in the automotive sector as

manufacturers strive to make lighter

and more fuel-efficient vehicles. The in-

vestments announced to date could in-

crease industry auto sheet capacity by

more than two billion pounds over the

next decade.

For more information, visit

aluminum.org/statistics.

26 26.6 25.3

22.7

18.4

20.9

22.7 23.9 24.3 25.5

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

North American Aluminum Demand

(Billions of Pounds)

Courtesy of the Aluminum Association.